26 May 2025

This year for the first time, large companies reported under the EU-CSRD harmonized framework. This recent regulation sets high and necessary standards for sustainability transparency, in particular regarding climate. Even though most companies see business benefits and are satisfied about the CSRD framework (See: this HEC study), voices recently called for simplification. To inform the debate, this article sums up key learnings from the first CRSD reports published by the BEL 20 companies.

In short:

Overview of the narrative elements

The 2024 CSRD-aligned reports from the BEL 20 companies reveal notable discrepancies, particularly in how companies address (semi-)narrative elements of their disclosures. Focusing on ESRS E1- Climate change, these qualitative components are intended to provide stakeholders with comprehensive information about a company’s climate strategy, transition plans, and the integration of climate considerations into business operations and financial activities. While some companies provide rich, detailed narratives, others remain vague, making it difficult for stakeholders to evaluate the robustness of their sustainability initiatives.

The role of digital tagging will be critical in improving the consistency, comparability, and accessibility of these reports. By adopting this technology, companies can better align with CSRD expectations and improve the overall effectiveness of their sustainability disclosures.

As the reporting landscape evolves, such advancements will not only help companies meet compliance requirements but also provide investors and stakeholders with actionable data that drives progress toward sustainability goals. It can even be a competitive advantage for reporting companies that can showcase their commitments and, more importantly, achievements in a clear data-driven narrative.

Carbon footprint

- Most BEL 20 companies have provided comprehensive data on their Scope 1, 2, and 3 emissions, with the GHG Protocol being the preferred reporting methodology. Almost all companies reporting their Scope 2 emissions provided location- and market-based figures.

- 80% of BEL 20 companies reported all GHG categories for Scope 3 emissions (or justified the exclusion of certain categories).

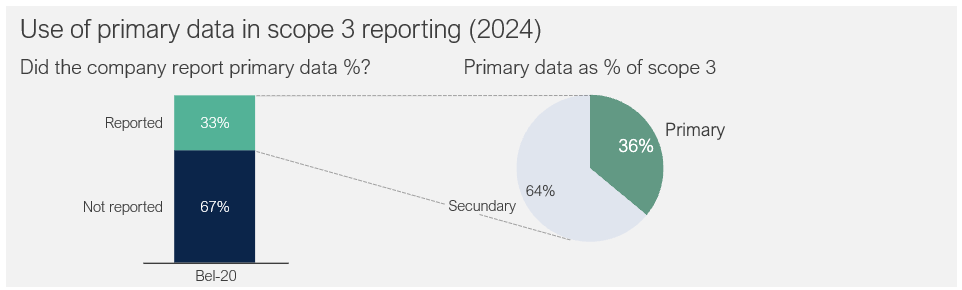

- Data quality still raises concerns: only one third of BEL 20 companies used primary data for calculating Scope 3 emissions. On average, these companies used primary data for just 36% of their Scope 3 emissions calculation.

Climact insights

A pragmatic data quality roadmap remains key to ensure that you can credibly measure the impact of your actions, such as supplier or client engagement, sustainable procurement strategy, eco-design, etc.

Transition plan

Reduction targets

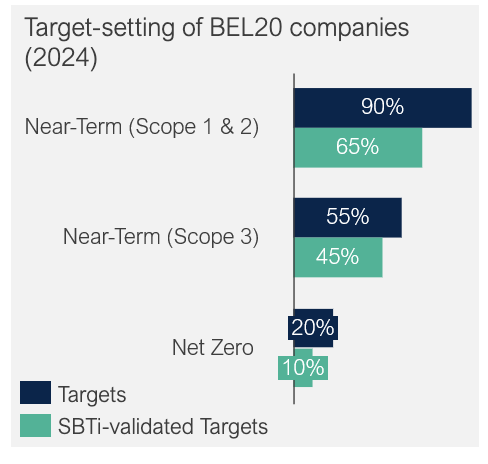

- Most BEL 20 companies have disclosed near-term mitigation targets for Scope 1 and 2 emissions, and a majority achieving SBTi validation for near-term goals. Strong momentum on Scope 3 with many planning to develop a Scope 3 near-term target.

- Over half have announced a net-zero ambition, but only a small minority have set long-term net-zero targets.

- ¾ of companies favor absolute reduction targets over intensity ones.

Incentives

- 55% report how climate-related factors influence board remuneration, with 30% linking ESG targets to pay through short- and long-term incentives.

- Less than 15% of BEL 20 companies have an internal carbon pricing scheme in place. Reported carbon prices range from €35 to €300 per tCO2eq, with typical schemes being shadow price (based on EU ETS or IEA) or internal fund.

Climact insights:

SBTi remains the strongest way to demonstrate a company’s commitment to the 1.5°C target. Having SBTi-validated targets offers a major strategic advantage by providing a rigorous, science-based framework recognised by over 10 000 companies worldwide. It strengthens credibility with stakeholders and supports long-term operational resilience.

Climate risks

Risks and opportunities (IRO)

- In the CSRD reports, most BEL 20 companies provide information on their risk management processes, although the depth of analysis varies significantly across companies. A majority assess physical and transition risks using either qualitative or quantitative methods.

- However, some companies are still in the process of developing internal frameworks to better manage their climate risks.

Financial impacts

- No company has reported on E1-9, which involves reporting anticipated financial effects from material physical and transition risks, as well as potential climate-related opportunities.

- Under ESRS E1-9, companies can omit the prescribed information for the first year (phase-in), which most of the BEL 20 companies did in 2024.

Climact insights

At Climact, we help companies translate climate exposure into financial metrics, turning scientific assessments into actionable insights based on best-in-class climate models. By evaluating both the cost of action and the cost of inaction, we build a solid business case for proactive climate strategies. The devastating floods in Belgium’s Vesdre Valley in 2021 caused €2.5 billion in damages, a stark reminder of the financial stakes. Across the EU, economic losses from climate-related extremes have reached €738 billion since 1980, of which €162 billion between 2021 and 2023 alone.

Our proven methodology supports companies, including some from the BEL20, in assessing climate risks and quantifying financial impacts, reinforcing resilience and informing decision-making.